Default Prevention.com (DefaultPrevention.com), was formed in 1998 to develop an efficient, economical ,

secure internet based default prevention program that integrates all Title IV participants into a single source

for default prevention; additionally to promote awareness and planning among schools, borrowers, and Title IV particpants.

Schools should see default prevention not only as a means to remain eligible to participate in Title IV programs, but also to serve

their student loan borrowers.

Even though this internet based program was created on the principle that students come first, the value of lowering the

default rate to schools should not be downplayed. The loss of federal aid affects both institutions and students.

This program is designed to work as a complete full service default prevention entity or to allow institutions to

utilize the DefaultPrevention.com infrastructure supported by institutional resources. In addition, DefaultPrevention.com provides training to help

schools implement the plan, or parts of the plan. Schools should also remember that once a default rate is under control, maintenance is

required to keep it that way. The DefaultPrevention.com plan, included at the end of this document, provides an example of a successful

default prevention program.

FLOOR PLAN FOR SUCCESS

Mission Statement

It is the mission of DefaultPrevention.com (DefaultPrevention.com), to provide *Front-End Driven ,

**Back-End Supported, web based default prevention systems and services to the higher education community and

qualified Title IV participants, in order to positively impact the repayment of student loans.

*Front End Driven- Front end processes are driven by institutional staff and currently attending students. In

addition to entrance interviews, all incoming students are required to provide 5 personal references which are verified;

additionally, financial aid personnel will use a national default prevention historical database to log phone numbers, addresses,

references, and related notes which then become available to other qualified Title IV participants.

** Back End Supported- Back end support provides the necessary resources to carry out a successful default aversion

plan by utilizing the data provided during the front end process. Including all communications with students, lenders,

guarantors, servicers, and institutional departments.

Getting to know individual students is a must. Ensuring that accurate data is collected, most importantly obtaining a minimum

of 5 valid references,

see“Reference Sheet”

. Collection and maintenance of current and historical student demograhpic information is paramount to

a successfull default prevetion program. Many schools wait until it is too late to determine their student information is

inadequate. The time to validate and verify student information is during the student’s attendance. References should all be verified

via a verification letter sent via U.S. Postal service. Students must be made aware of this procedure up front. On many occasions references

will contact the school in regards to the reference letter and indicate their support for the student.

NOTE: “You get what you inspect, not what you expect.”

High risk students are likely to provide references that are invalid. Students must be made aware that their references will be verified;

therefore, students should be encouraged to take extra time in completing the reference sheet accurately.

“Emergency Contacts”, Students first day of attendance is filled with excitement and anticipation. Schools should

use this as an opportunity to complete additional references via an “Emergency Contacts” form. Amazingly, these references are many

times unique from those provided on the “Reference Sheet”

.

Additionally, it is important for financial aid officers to know the student population in general, as well as the institutional

and demographic variables of student loan defaulters.

Who Are Your Student

Analyze the studea is Everythingnt population.

- Enlist the aid of professional statisticians on the faculty or at a guaranty agency.

- Request student data from the school’s computer center or from a guaranty agency.

Identify any common characteristics between:

- Defaulters and non-defaulters, and

- Borrowers and non-borrowers.

Examine institutional variables including:

- GPA

- Income,

- Year in college,

- Class, and

- College entrance scores.

Examine demographic variables, such as:

- Student population by county,

- County employment and unemployment rates, and

- Per capita income by county.

Look at your student data on regular basis

Title IV Participants-Lenders and Servicers

Track the performance of each servicer and lender.

- Use DefaultPrevention.com’s lender and servicer cohort default rate estimates to:

- Benchmark servicers on their default rate, and

- Benchmark lenders on their default rate.

Compare the performance between servicers based upon:

- The number of claims filed per month, and

- The number of claims paid per month

Identify problem areas.

Identify “best practices” among servicers.

Compare apples to apples and apples to oranges

Track the performance of the university, college, or proprietary school’s default management plan.

- Benchmark the institution’s default rate with similar institutions. Gather data from

- DefaultPrevention.com’s reports (www.defaultprevention.com) and

- The Department of Education web site (www.ed.gov).

- Identify how differences between the institutions related to differences in the default ratios.

- Track the present cohort default rate using the following calculation (for schools with more than 30 students entering repayment):

Numerator

_________________x 100

Denominator

Numerator = Number of students who entered repayment during the

fiscal year and defaulted within that fiscal year or the subsequent fiscal

year

Denominator = Number of students who entered repayment during

the fiscal year.

Project future rates using DefaultPrevention.com’s Estimated Cohort Report (ECR) to take action to minimize the default rate.

A ECR lists all borrowers at a school who entered repayment during a specified fiscal year and provides3.

repayment status for each borrower. Quarterly ECR’s are available in the reports section online at www.defaultprevention.com/

Address High Risk Students

Reallocate a portion of state and institutional grants to award potential defaulters.

Reallocate a portion of work-study funds to award potential defaulters.

Promote scholarships.

Promote conservative borrowing.

Offer comprehensive counseling services:

Meet one-on-one with potential defaulters who are requesting loans in order to limit debt by determining the student’s eligibility for other gift aid such as:

- AFDC exemptions

- State or institutional grants

- Scholarships

- Work-study, and/or

- Educational aid exemptions

Identify the “real costs” of a higher education.

Prepare a realistic budget with the student.

Discuss expenses and money-saving strategies.

Analyze salary surveys.

Hire an “Owner”

(Someone who will take ownership in your default rate)

Every financial aid office should hire/assign a full/part time professional to function as a default prevention officer. Ownership of the default rate should be discussed

and this person is responsible for researching and forecasting default rates. Ownership is nothing more than accountability.

General Job Description

The designated default prevention officer should take ownership in your School’s default rate.

This can be a part/full time person depending upon the size of your School. The duties of the this person may include.

- Administer the institution’s default prevention program;

- Serve as a financial aid advisor for an assigned caseload of student aid recipients;

- Serve as a liaison between the office of student financial aid and other campus departments, parents,

and outside agencies such as student loan lenders, servicers, guaranty agencies, and the Department of Education (ED);

- Render decisions and oversee processes requiring initiative and judgment in responding to the individual needs of students;

- Develop the information needed to prepare reports required by financial aid programs;

- Counsel and advise students regarding their financial options and responsibilities;

- Supervise employees in administration of the school’s default prevention program;

- Manage pre-claims assistance efforts such as telephone and letter campaigns;

- Handle pre-loan and exit-loan counseling and implement enhancements to the prcedures;

- Supervise and perform statistical analysis for internal and external reporting;

- Track the school’s cohort default rate;

- Interpret and implement regulations set forth by ED and state guaranty agencies; and

- Oversee the timely completion of deferments and enrollment history requests by working

closely with the registrar’s office or assuming the responsibility in the financial aid office.

The position recommends the following education:

- A bachelor’s degree in a field related to the default prevention program, such as

business, communications, or social work. Or substantial financial aid experience.

Position experience should include:

- Two to three years experience in the appropriate field of the program with two years of responsible administrative experience.

- Preferred two to three years experience in student financial aid loan programs and related outside agencies such as lenders, servicers,

guaranty agencies, and ED.

- Working knowledge of internet, email, instant messaging, internet browser, database, spreadsheet, and presentation software as well as

computer hardware.

The Default Prevention Officer must possess the following skills:

- Excellent writing skills,

- Communication skills,

- Interpersonal skills, and

- Organizational skills.

The Default Prevention Officer must be able to:

- Analyze data,

- Forecast and plan,

- Work under pressure,

- Solve problems, and

- Accept and implement change.

Educate your Borrowers

Providing comprehensive entrance and exit counseling sessions is an excellent way to educate students on the rights and responsibilities of borrowing a student loan. This type of interactive session creates an environment in which the borrower can ask questions and voice concerns. Requiring students to

attend yearly review sessions will reinforce the information covered during the entrance counseling session.

Spruce up your Entrance Interviews

- Invite loan specialists, lenders, and servicers to present at the sessions.

- Distribute materials containing loan information to the borrowers for future reference.

- Delay certification of loan applications until first time borrowers have attended a session.

- Offer sessions intermittently throughout the semester to promote attendance.

- Offer one-on-one entrance counseling to students who cannot attend group sessions.

- Use entrance counseling features on http://www.mapping-your-future.org/services/oslchow.htm .

- Test borrowers at the end of the session to identify students who may need additional counseling.

- Use test results as an indicator that all relevant information is being covered during the session.

- Discourage multiple lenders and guarantors.

- Provide students with disclosure statements that contain the following information:

- Cumulative amount borrowed,

- Estimated interest, and

- Estimated monthly payment.

- Provide students with loan summaries.

- Update students on changes in financial aid office procedures.

- Remind students of their rights and responsibilities.

Gather updated information from students, including:

- New addresses and telephone numbers,

- Changes in their permanent addresses,

- Reference information, and

- Employment information.

Cover the consequences of default.

Delinquent Borrowers- Talk to Them

- Counsel and assist delinquent and/or defaulted borrowers either in person or over the phone.

- Act as a liaison between the student and the lender, servicer, and/or guaranty agency.

- Facilitate the completion of documents such as deferments and forbearances.

Educate delinquent borrowers on repayment options:

- Standard repayment plan,

- Graduated repayment plan,

- Income sensitive repayment plan,

- Repayment incentives offered by servicers, and

- Consolidation.

Educate defaulted borrowers on repayment options:

- Regaining eligibility for Title IV aid,

- Loan rehabilitation, and

- Consolidation.

Counsel excessive borrowers

(to be defined by the individual institution) on a one-on-one basis about:

- Responsible borrowing

- Budgeting

- Debt management plans

- Repayment options, and

- Salary expectations

Exit Counseling

- Invite lenders and servicers to present at sessions.

- Include and emphasize the correct procedures transfer students should follow when notifying their lenders that they have transferred

and in filing deferments.

- Provide students with a loan summary that includes the names and phone numbers of lenders, servicers, and guaranty agencies.

- Offer one-on-one exit counseling to students who cannot attend group sessions.

- Let students know they can call the school for assistance; provide them with the name and phone number of a contact person.

- Verify that all exit interview forms are completed in full.

- Administer an exam at the end of the session to identify students who may require additional counseling.

- Send borrowers a letter or brochure during their grace period reminding them of their rights and responsibilities and listing phone

numbers to call for assistance.

Frequent Updates

REMEMBER TO UPDATE

www.defaultprevention.com

ONLINE DATABASE WITH

ALL CHANGES IN:

ADDRESS

PHONE NUMBERS

REFERENCES

Title IV Partnerships Your Key to Success

For an institution to combat a default rate problem, it must have the support of its own campus in addition to lenders, servicers, and guaranty agencies. 3

Forging alliances facilitates efficiency, learning and promotes progress.

- Include and emphasize the correct procedures transfer students should follow when notifying their lenders that they have transferred

and in filing deferments.

Your data is now available to your lenders, and guarantors

via your web-based online default prevention program.

www.defaultprevention.com

THIS IS HUGE!

Partnerships and Alliances

College Departments

Study Your Data Regularly

Registrars Office

Lenders

Placement Office

Servicers

Guarantors

ED

Close the Gap with Other Campus Departments to Promote Default Prevention

- Emphasize to the registrar’s office the importance of cooperating in a timely manner

and skip tracing requests, address changes, etc…

- Ensure that every department utilizes www.defaultprevention.com for updates of student addresses, phone numbers, personal

references, etc….

- Make default prevention a priority for the entire financial aid office by educating all departments.

- Invite placement office counselors to present at exit sessions.

Partner Up with Outside Agencies to Promote

and ASSIST in your Default Prevention

Take advantage of services offered by lenders, servicers, and guaranty agencies such as:

- Online account access

- Electronic delinquent borrower reports

- Online entrance and exit counseling

- Assist with contact management activities.

- Develop a relationship with guaranty agency representatives to communicate any special needs in dealing with delinquent or defaulted borrowers.

- Assign a “Hot Line” person to process and expedite special situations that

students about ready to default.

Be a Techie

Effective use of technology simplifies processes, which in turn saves time and labor.

- Use the online reports offered by www.defaultprevention.com.

- Log on to the National Student Loan Database (www.nsldsfap.ed.gov) for student information.

- Learn and use instant messenger services; i.e.,Messenger, AIM , ICQ.

You may decide to use these services for inter-office messages.

- Consider placing “live help” on your website for student inquiries

- Gain user id’s and passwords to each lender and servicer web access site.

Cyber Connections Get Them or Bust

- Create a financial aid web page for students to view and use as a reference, with forms on line.

Or go to www.defaultprevention.com for appropriate links.

- Provide links for students to other financial aid and scholarship sites.

- View and print loan summaries from Adventures in Education (www.AdventuresInEducation.org) to distribute to students at exit counseling sessions.

- Download default reports offered by lenders and servicers.

- View and print account information from servicers who offer this information over the Internet.

Download and print deferment and forbearance forms, or go to www.defaultprevention.com on line .

- View and use Estimated Cohort Default Reports to identify delinquent and defaulted borrowers to begin default prevention efforts.

- Provide computers for students to use, either in the lobby of the financial aid office or in a lab setting, to access

their account information online.

E-mail – The Only Way to Communicate

- Ensure that all financial aid personnel have and use institutional email addresses.

- Disallow use of second tier email addresses; i.e, aol, msn, yahoo, hotmail.

- Upon termination ensure that all emails are forwarded to the administrator. This ensures that future emails

are opened and read by a supervisor.

- Use e-mail to communicate with borrowers and/or parents in the form of newsletters on a semester basis.

- Ask the school’s administration to allow students to use their school e-mail addresses for up to two years after leaving

school to keep in contact with borrowers,

- Encourage students to use e-mail as a way to communicate with financial aid office staff.

- Instant messaging, get it, learn it, because it’s coming to your school soon.

Service Fees

Default Prevention.com provides you with two service options.

Full Service: We do everything. (Recommended for schools with an official cohort rate above 17.9%). We provide the plan, labor, resources,

contact management efforts, correspondence resources, etc.)

Platform Service: We provide you with web access and electronically download your delinquent borrower reports.

You provide the labor and resources necessary to carryout default prevention activities.

(Ideal for schools with a designated institutional default prevention person combined with three consecutive official cohorts under 15%). .

- Site access, up to 20 users.

- Database access.

- Training and support, (see support schedule).

- Electronic monthly delinquency data import.

- Daily delinquency reports.

- Daily cohort reports.

- Daily loan status reports.

- Full web site and data access.

The Resource Factor is determined to be an approximation of the anticipated amount of labor and resources utilized to perform

full default prevention services as outlined in the default prevention plan. Resource Factor is currently (3.0). For example,

resources and labor relating to the following:

- Data entry.

- In school servicing of references and reference verifications.

- Grace period servicing.

- Delinquency servicing, written and verbal.

- contact management services, written and verbal.

- Forbearance/deferment processing written and verbal.

The costs of implementing a sound default prevention program vary depending on which default prevention tools the institution chooses to

implement. Costs fall into two categories:

Resource expenses associated with developing the default prevention program:

- Workstations equipped for internet access

- High speed data connections, internet access

- Training

Resources associated with the day-to-day operation of the default prevention program:

- Personnel costs such as wages

- Supplies

- Paper

- Envelopes

- Postage, and

- Postcards

- Overhead costs

- Telephone service

- Long distance

- Utilities

- Maintenance

- Training and Support

Training and Fees

Default Prevention.com provides you with training and support according to the following schedule.

The system is simple to use and most schools are up and running well within the first month.

Challenges and Appeals are available on case by case basis. Email mattk@defaultprevention.com for consultation and quote.

Case Study

I. Case Study-Cohort Problem

1996

A nationwide mulit-campus Financial Aid Office is in crisis due to the

FY 1996 Cohort Default Rate of 17.3%.

II. Case Study -Current Program Analysis

- No designated default prevention specialist existed.

- Default prevention plan existed with minimum requirements.

- Partnerships with Lenders and servicers was non existent.

- Electronic communications of default related reports were unavailable.

- Internet access from financial aid office was insufficient.

- Reference gathering and verification techniques were not being used.

III. Case Study-Solution

Default Management Plan

Internet based default prevention application

Gather and verify 5 personal references.

Assign a default prevention person

Build partnership with lender and servicer

The College employed the services of Default Prevention, Inc. to implement

a proactive approach to default prevention at their Las Vegas campus to include emphasis in the following main areas:

Additional modifications included:

A. Change packaging philosophy:

- Offer a grant in lieu of a loan for entering freshman first-time borrowers, since the statistical analysis proved freshmen

were responsible percentage of defaults.

- Do not award students Perkins loans and Stafford loans in the same award package (unless documented professional judgment is included).

Personnel were assigned as :

- Default Prevention Officer, (10 hours per week).

The responsibilities of the default prevention area were enhanced to include:

Comprehensive counseling services for borrowers:

- Excessive borrowers

- Delinquent and defaulted borrowers.

- Provide pre-claims assistance to students to prevent technical defaults (i.e., provide deferment forms).

- Promote grants, part-time jobs, and scholarships.

Use of delinquency/default information tracking tools:

- Use DefaultPrevention.com’s monthly Default Prevention Estimated Cohort Reports.

Generation and printing of delinquent borrower letters. The students who appeared on these lists are called and offered assistance in

dealing with their delinquent loans .

Generation and printing of monthly delinquent letters. Letters included a listing of the consequences of default,

as well as the name and phone number of the servicer the student needs to contact, were sent to delinquent students.

Phone calls to delinquent borrowers.

- Calls were made to students who are 150-days and above delinquent to offer them assistance and guidance related to their delinquent

loan.

- Calls were also made to references.

Improvements in the process for Deferments/Enrollment Verification requests. The financial aid office

assumed the processing of deferments and forbearances that previously were filed by the admissions office to ensure

completion in a timely manner.

Processing change-of-address requests from lenders, including re-sending returned mail.

Alliances built with guaranty agency, lenders, and servicers:

- Obtain lenders that will cooperate with electronic and customer service issues.

- Eliminate lenders that will not accommodate student forbearance deferment requests online.

- Guarantors:

- Obtain guarantors that provide a monthly delinquent borrower report, cumulative.

Electronic linkages/Internet access:

Gain user ids and passwords to all Title IV participants that service the

Provide all financial aid staff with internet access.

Access to the Internet is an important tool DefaultPrevention.com uses to fight default.

- Borrower information is available at DefaultPrevention.com.

- Access to borrower data from lenders/services.

- Delinquent borrower reports on line at DefaultPrevention.com.

F. Enhanced entrance and exit loan counseling

Lenders and servicers are involved in loan counseling sessions.

Pre-loan counseling sessions provide more information on the Stafford Loan Program and emphasis is placed on the responsibility of the borrower.

Certification of first-time borrower loan applications is delayed until a student successfully completes a pre-loan counseling session, and 5 verified reference, see form on next page.

The pre-loan test is continuously reviewed for enhancements to test a student’s knowledge of a borrower’s rights and responsibilities.

A student must pass the test to receive credit for attending the pre-loan counseling session.

Exit counseling sessions have been improved to provide more information on a student’s rights and responsibilities once he or she enters repayment.

At the beginning of the exit loan counseling session, a student is given a summary of his or her loans printed from DefaultPrevention.com’s web site.

At the end of the exit counseling session, students take a test that helps to identify those who may need additional counseling.

Default prevention intervention techniques generally take two full cohort reporting periods to see results. As in the above case study,

procedures and policies that were implemented in 1996 and 1997 impacted the default rates in 98 and 99. Schools should not look for

immediate cohort improvements. Immediate results can be viewed in the number of delinquent borrowers showing

up on reports and how those delinquent borrowers are progressing towards claims status.

- default management plan was implemented, there was a 93 percent decrease in the default rate the last four

years and a net decrease of 16.2 percentage points.

- This is a dramatic improvement and each school will experience different results. Past performance is no guarantee for future performance

Example of Delinquency Progression

Good Trend

Good Trend: Illustrates students entering delinquency status in the early stages and then falling off as they progress towards default.

Bad Trend

Bad Trend: Illustrates students entering delinquency status at the same pace; however, they are all progressing towards default at

an equal pace

V. What’s Ahead

- DefaultPrevention.com will continue to evaluate and analyze its default prevention area to improve its success in addressing the issue

of default prevention

- Developing teleprompting for data input and retrieval from voice recognition software.

- Creating online debt management seminars for DefaultPrevention.com students.

- Automating deferments and enrollment history process.

- Providing instant messaging capabilities for all members.

- Continuing to build alliances with other agencies in the student loan industry.

Development:DefaultPrevention.com has developed a highly effective, and secure, website for the purpose of allowing approved parties

access to borrower information via an internet connection. Internal and external resources are utilized to accomplish this goal. Database

populations are imported from institutional data transfers and disseminated to DefaultPrevention.com participants via www.defaultprevention.com

Deployment/Training: Deployment of database product is as follows:

- Database population are imported from participating DefaultPrevention.com institutions.

- Training at the institutional level on read/write and data entry, by DefaultPrevention.com.

Security:

- Data Security: The most current encryption tools are used to safeguard the data. Secure servers and experienced providers will host the site.

- User Interface: Participants will have to be approved prior to accessing the data.User ID’s and passwords are assigned to

approved individuals.

- Browser Compatibility: 128 bit cipher strength required, Explore 6+ recommended.

Replication: Database replication is as simple as an institutions decision to adopt this tool as part of their default aversion policies and procedures. DefaultPrevention.com

then imports their data and the site provides tutorials and help screens to walk users through the different areas of the site.

Innovation: Innovation is the driving force behind DPI. Data driven websites are on the forefront of website development. Dynamic websites

are those sites that allow read/write abilities over the internet. This technology in the Title IV community has been available for some time; however, an institution’s

ability to allow others access to their borrowers data has been non existent. Having access to information is key to any default aversion program, at every level. Communication of borrower information is the frontline of default aversion programs, and DPI allows real time access to data on the desktop. The ability or inability to obtain information from all parties is directly related to defaults.

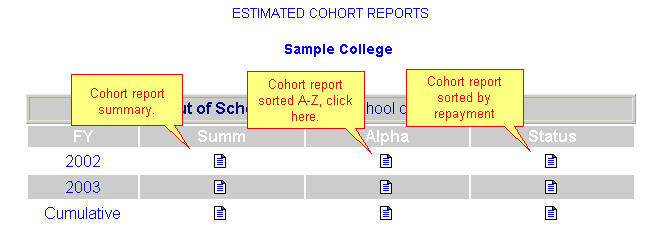

REPORTS

Reports Link

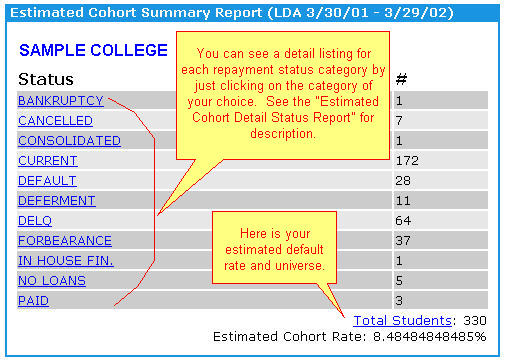

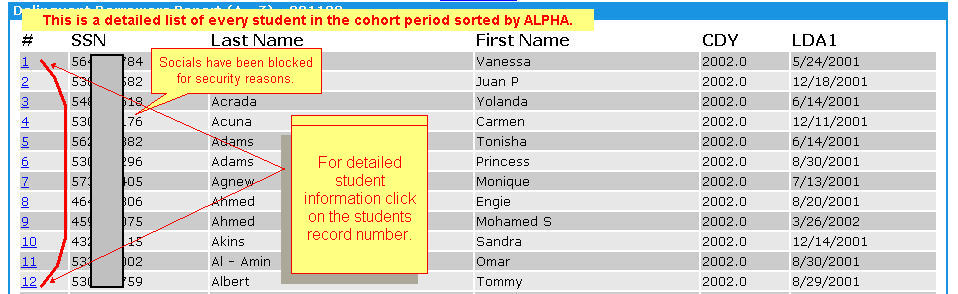

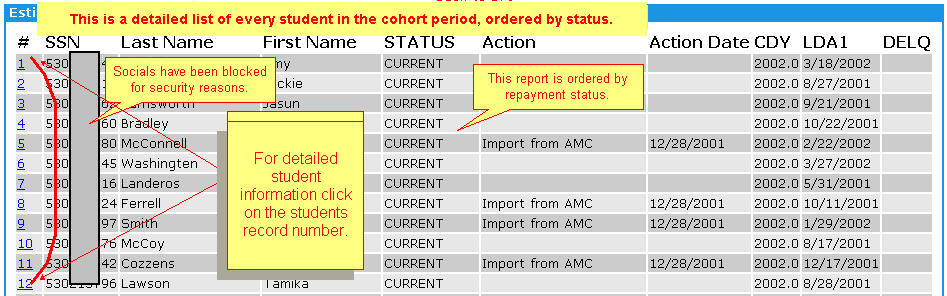

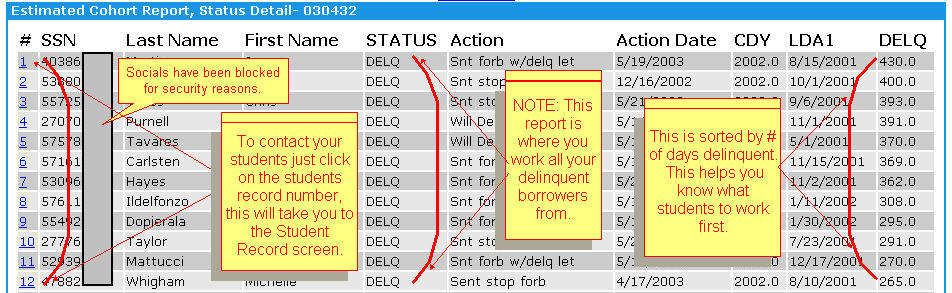

Estimated Cohort Reports

Than bese reports ce used to:

- Define a repayment cohort and calculate a cohort default rate.

- Monitor a school’s month-by-month cohort default rate progress.

- Help to forecast a school’s cohort default rate.

- Identify delinquent borrowers for targeting with default prevention resources.

- Contact borrowers using the address and phone number information. Click on each status for a detailed list of students.

Estimated Cohort Report by SUMM

Estimated Cohort Report by ALPHA

Estimated Cohort Report by STATUS

Detail Status (delinquency) Report